6 Jun 2026

Decoding How Encryption Protocol Updates in Card Platforms Align with Shifts in Cross-Border Transaction Compliance and User Verification Timelines

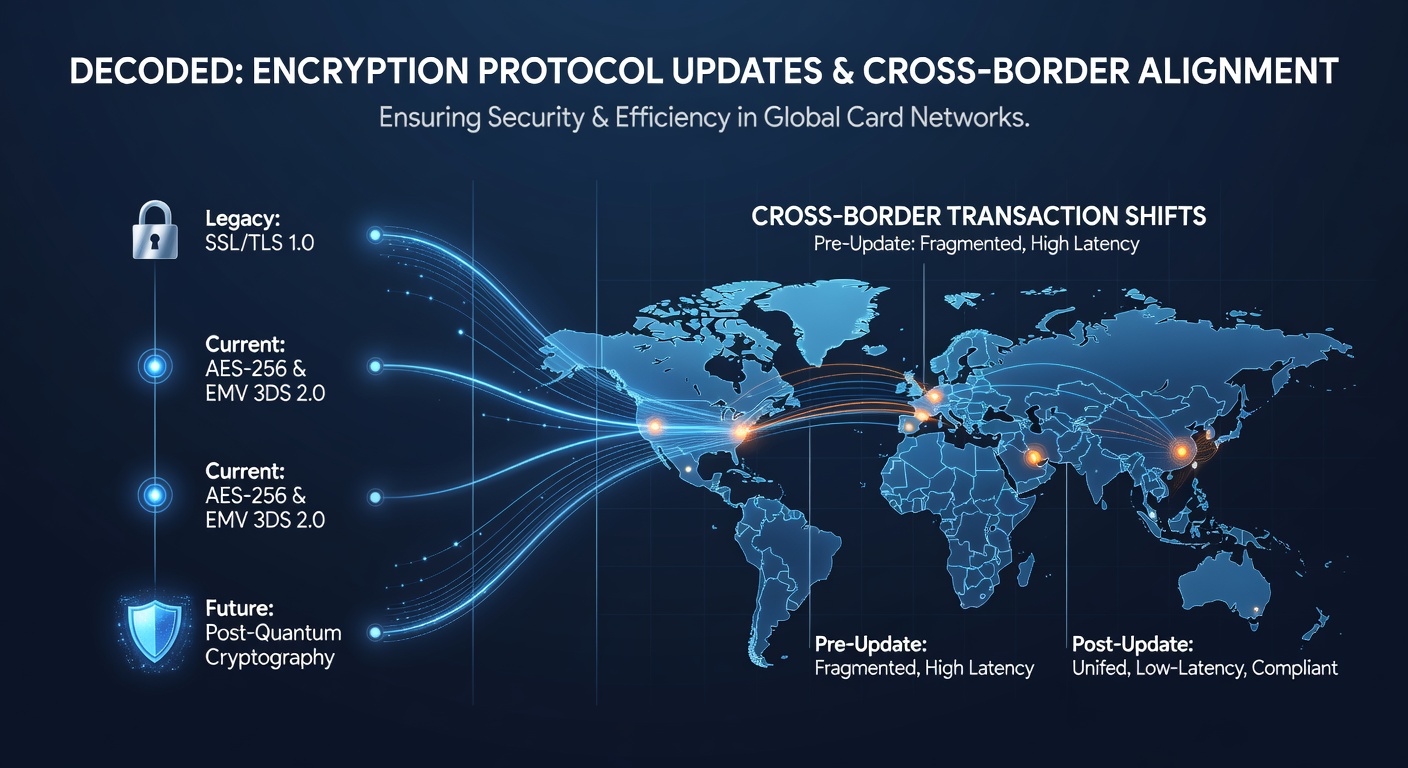

Card platforms continue to refine their encryption protocols as regulatory frameworks for cross-border transactions evolve, and observers note that these adjustments often coincide with new requirements for user verification timelines. Data from payment security councils shows that updates to standards such as TLS 1.3 and advanced AES implementations have accelerated since 2023, driven by mandates that demand stronger protections for data in transit between jurisdictions.

Researchers at institutions tracking financial technology report that platforms handling international card payments now integrate quantum-resistant algorithms in pilot phases, while compliance deadlines push verification processes into shorter windows, sometimes requiring completion within 48 hours of transaction initiation. This alignment appears in multiple regions where financial intelligence units coordinate their rules with technical security benchmarks.

Encryption Protocol Evolution in Digital Card Systems

Encryption updates follow a pattern where major protocol changes roll out in tandem with compliance reporting cycles, and figures from industry audits reveal that card platforms adopting end-to-end encryption see reduced exposure during multi-jurisdictional transfers. Take one platform operating across North American and European corridors that completed migration to TLS 1.3 by early 2025, allowing it to meet verification deadlines set by updated anti-money laundering directives without extending user onboarding periods.

Those who monitor these systems point out that legacy protocols like TLS 1.2 receive deprecation notices at the same time new verification layers activate, creating synchronized implementation schedules. Evidence from transaction monitoring reports indicates that platforms completing these upgrades experience smoother alignment with data localization rules in regions such as Australia and Canada.

Cross-Border Compliance Adjustments and Their Technical Triggers

Shifts in cross-border rules often originate from coordinated efforts among regulatory bodies, and the Financial Transactions and Reports Analysis Centre of Canada has outlined verification timeline compressions effective through mid-2026 that directly reference encryption strength benchmarks. Platforms respond by embedding automated key rotation mechanisms that match the frequency of compliance audits, reducing the lag between policy announcements and technical deployment.

What's interesting here is how June 2026 marks a convergence point for several overlapping deadlines, including enhanced due diligence requirements for high-value international transfers that now stipulate real-time encryption verification alongside identity checks. Data shows platforms that pre-aligned their protocols avoided bottlenecks during these periods, whereas others faced extended verification queues.

Industry reports from research organizations document cases where card platforms integrated zero-knowledge proof elements into verification flows, allowing compliance teams to confirm user details without exposing raw data across borders. This approach supports shorter timelines while satisfying encryption mandates from multiple authorities simultaneously.

User Verification Timelines and Protocol Synchronization

Verification timelines have tightened in response to encryption advancements, and analysts observe that platforms now trigger identity confirmation sequences immediately after protocol handshakes complete. According to transaction data compiled by the Australian Transaction Reports and Analysis Centre, average verification windows contracted from five days to under 72 hours in systems that deployed updated encryption suites by late 2025.

Yet the synchronization extends beyond timing, as new protocol versions often include built-in hooks for compliance logging that feed directly into regulatory reporting portals. People who oversee platform operations note that these features eliminate separate data extraction steps, letting verification and encryption compliance occur within the same operational cycle.

One study from a European research consortium revealed that card platforms using unified frameworks for both elements achieved higher consistency in meeting cross-border deadlines compared to those managing them separately. The patterns suggest continued convergence as more jurisdictions adopt similar technical standards.

Regional Variations in Implementation

Implementation differs across regions while maintaining core alignment principles, and platforms serving Asia-Pacific markets have incorporated encryption updates alongside verification rules issued by local financial authorities at a pace that matches European schedules. Observers tracking these developments find that shared technical standards facilitate smoother cross-border flows even when local timelines vary slightly.

Take platforms that operate under both Canadian and Australian oversight, where encryption protocol refreshes coincide with verification mandates that became stricter in 2025. Records indicate these entities complete updates in coordinated phases, ensuring transaction data remains protected during the compressed compliance windows.

Conclusion

Encryption protocol updates in card platforms continue to track closely with changes in cross-border transaction compliance and user verification timelines, producing operational patterns that researchers and regulators document across multiple jurisdictions. As standards mature through 2026, platforms that maintain this alignment demonstrate measurable consistency in meeting technical and regulatory benchmarks simultaneously. The interplay between these elements shapes how card payment systems handle international data flows under evolving requirements.